Incorporation helps many owners pool their investments into shares of a single firm. As legal fictions, corporations are able to sign contracts and outlive any individual owner, and limited liability means that owners can't lose more than the money they put in to their stock. But as legal persons, corporations are also expected to pay tax on their profits, and since World War II, this tax rate has been significant.

Corporations tend to be larger than other firms: Fewer than one in five business firms are incorporated, but these account for over 80 percent of sales. The federal corporate income tax currently begins at 15 percent, quickly rising to 35 percent for profits over $18 million - though the marginal rate actually rises to a high of 39 percent for profits up to $100,000, so that the average catches up to 35 percent. In addition, all but a handful of states charge their own income taxes on corporate profits, as do some municipalities. California charges a flat 8.8 percent, while in Iowa the maximum rate reaches 12 percent. Nevada's rate, of course, is zero.

Even ignoring state and local taxes, the 35 percent federal rate is higher than in many other countries. China and Germany, Mexico and Canada, the United Kingdom and even France have lower tax rates than this. Of the major economies, only Japan has a higher tax rate.

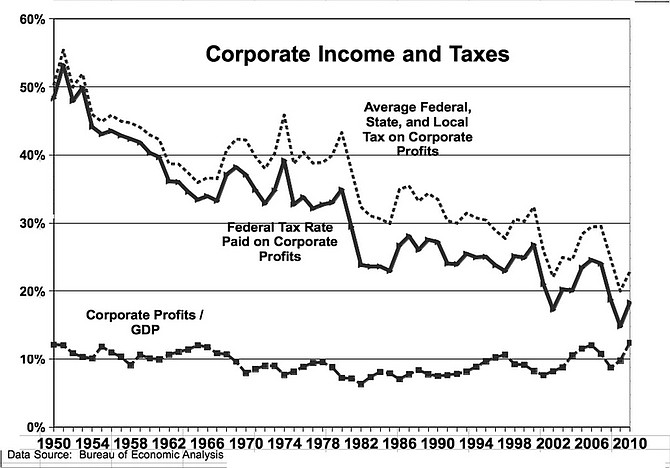

But there is a significant difference between the statutory tax rate and the rate corporations actually pay. In fact, over the last five years, American corporations actually paid about 20 percent of their reported profits to the federal government, and another 5 percent to state and local governments. Corporations have access to many tax credits, especially the foreign tax credit, and they have many ways to shelter income from taxes, including access to offshore havens. They can even deduct the value of the stock options they give to their top executives.

As a result, the actual tax rate paid is the lowest it has been in 60 years. During the Eisenhower presidency, profit taxes were twice as high. Even during the Reagan administration, after the top rate was dropped from 46 percent, corporations paid a significantly higher rate.

Since stockholders pay personal income tax on their dividends or on their capital gains (albeit at a much lower rate), profits are essentially double-taxed. Any corporate tax cuts would filter down to the stockholders in the form of higher dividends or capital gains. While many people own some stocks, it is estimated that the entire corporate tax burden is less than 2 percent for the bottom 80 percent of income earners. For the top 1 percent of income earners, however, the tax burden rises to about 9 percent of income, since most of their income comes from what they own, not what they do. Thus, some argue, profits taxation is unfair. That is a point upon which reasonable people may disagree.

The better question is, does the corporate income tax discourage profitable activities? In choosing between investments in two different locations that are otherwise identical, the marginal profits tax might matter. If so, we might expect there to be a negative correlation between the tax rate and the relative amount of profits earned in this country.

However, corporate profits as a share of Gross Domestic Product have not shown much of trend either way. Profits peaked at 12 percent in 1965, fell to a low of 6.3 percent in the recession of 1982, and then bounced back. Last year, profits reached a postwar high of 12.4 percent of GDP, even though the economy was still weak. To the extent there is correlation between taxes and profits, it is positive, not negative, because causation goes the other way. When profits are up, the average tax rate paid rises too.

Still, the fact that the American corporations pay less in tax now than anytime in 60 years might be related to current record profits. Perhaps lowering corporate rates to new postwar lows could lead to new postwar highs for corporate profits, and perhaps some of those profits might come from actual investments that increase employment, rather than from downsizing or speculative trading. Perhaps, but it doesn't show up in the postwar data.

We already have a large federal budget deficit. Federal receipts have fallen to the lowest share of GDP we have seen since the 1950s. While corporate income taxes are only 10 percent of federal revenues, any more revenue cuts will just add to the growing federal debt. We will eventually have to face up to that, and any more tax cuts will have to be offset by other types of taxes, such as those on personal income. We could try to make revenue-neutral changes to the tax code, to decrease the statutory 35 percent rate while eliminating corporate tax breaks, but we did that already in the 1980s, and innovative accountants are likely to soon find new ways to reduce taxes.

Are corporate tax rates too high? It depends on your perspective - and unfortunately, that perspective seems to be sorely lacking.

• Professor Elliott Parker is chairman of the Economics Department at the University of Nevada, Reno.

Comments

Use the comment form below to begin a discussion about this content.

Sign in to comment